Laboratory products

Published over 5 years ago. See the latest and most current information on Laboratory products.

One of the most confusing issues for laboratory purchasers and suppliers alike is whether or not VAT should be charged on equipment for research bodies. HMRC recently raised the spectre of suppliers and research labs having to go back over years of accounts to identify items which might have been wrongly charged, when it released new guidance which set the industry’s previous understanding on its head.

If you are a university or charity carrying out medical or veterinary research using charitable funds, you can buy most of your laboratory equipment without paying VAT on it. The 20% VAT is significant since it is usually not recoverable by universities and charities. Lab equipment has evolved from what was available when the law first came into effect and after years of changes and minor additions to and subtractions from the guidance, much modern lab equipment is not explicitly listed in the HMRC guidance which states:

“This list is not exhaustive. With the pace of technological change, new types of equipment will often be developed. If an item does not appear on this list, the underlying principles set out in this notice should be followed to determine if the item is a qualifying one. In areas of doubt, specialist advice should be sought.”

Unfortunately, the underlying principles are not set out, and suppliers and purchasers have to use the wisdom of Solomon to try to decide what rules to infer from the morass of conflicting and confusing guidance.

Anomalies include the fact that while glassware is generally eligible, plastic equivalents are not, re-usable lab coats are eligible, but disposable ones are not, and the guidance is particularly unclear when dealing with bulk substances.

The whole area of PPE is particularly confusing - can it be eligible as an accessory to equipment if the equipment can’t be used without it? Or is it equipment in its own right? It used to be that medical standard PPE was eligible for zero rate VAT, but the last HMRC guidance suddenly said that Nitrile gloves were not eligible under any circumstances. Until the end of October of course, because of COVID-19, all PPE is zero rated for VAT, but will you be charged VAT on PPE purchases after that or not?

Some universities have recently engaged consultants to pursue VAT refunds on past purchases where it is possible that these should have been zero rated for VAT, but even for VAT inspectors the existing HMRC guidance poses more questions than it answers, so such queries are likely to take some while to resolve. Long-running arguments over past VAT aren’t in the interests of either the charities or the lab suppliers although they might possibly benefit their respective solicitors.

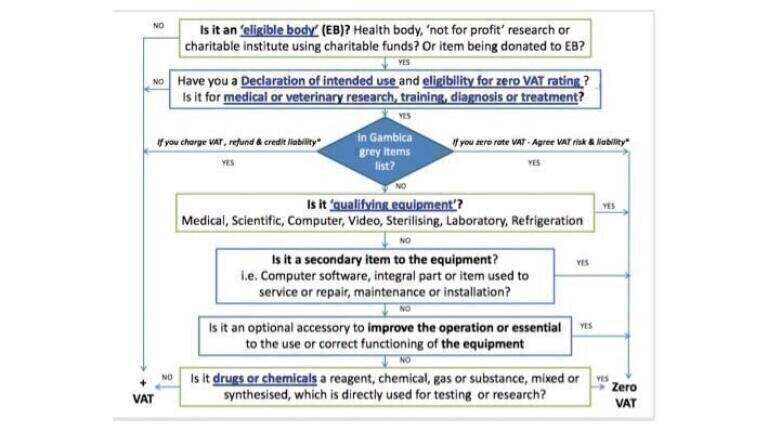

Amid all the confusion, a group of expert GAMBICA members including, Camlab, Thermo Fisher, Starlab, VWR and Appleton Woods have come together to form a VAT group to provide the specialist advice mentioned in the guidance but not actually available until now. They have developed clear, comprehensive guidance which will help all parts of the industry make consistent decisions about VAT.

The guidance consists of a short, clear precis of the law and guidance covering VAT on laboratory supplies with links to all the relevant documents and,

• a decision-making flowchart to help suppliers and customers put in a consistent process for charging or not-charging VAT, and

• a list of 109 ‘grey items’ where the guidance remains unclear.

These ‘grey items’ are subject to further debate and consultation with HMRC but GAMBICA’s VAT group has listed items where the HMRC guidance is contradictory or unclear and set out a rationale for these items being either eligible or not for the zero-rating relief. Of course, it is still the suppliers’ decision as to whether to charge standard or zero rate VAT.

One item on the ‘grey’ list is diagnostic and research kits. The HMRC guidance on these is unclear but the VAT group suggests they may be eligible as: These kits could contain a mixture of equipment and chemical reagents such as enzymes and antibodies. These kits are specifically designed for use in a laboratory. ‘Drugs and Chemicals/Substances’ are covered under HMRC guidance note 701/1 under (6), ‘VAT relief charities can obtain on their purchases’. In section 6.1.4 ‘Drugs and Chemicals’ defines ‘substances’ as (natural or artificial, solid, liquid or gas or vapour) in whatever format (natural or artificial, solid, liquid or in the form or gas or vapour) directly used for testing or for mixing with other substances in the course of research.

GAMBICA’s VAT group advises that all suppliers and purchasers agree between themselves how items on the grey list will be treated for VAT and how the liabilities will be managed should any decision prove later to be incorrect.

This guidance is now available to GAMBICA members on the GAMBICA website here: https://www.gambica.org.uk. If you are not a GAMBICA member, please email me at [email protected] and I will be happy to send you a copy.

GAMBICA hasn’t stopped at that however. Chief Executive, Steve Brambley, has sent the guidance to HMRC and is seeking a meeting to gain an HMRC position on items on the ‘grey’ list. He is also pressing for a wider interpretation of the original law noting that all those who donate funds to charity, do not expect the chancellor to grab a fifth of it back in VAT.

In particular he has recommended that all PPE used in charitably funded medical and veterinary research be eligible for zero rate VAT and that eligible bodies be allowed to claim zero rate VAT on all equipment used in research, treatment or training.

He argues that although there would be an exchequer cost to allowing more items to be eligible for zero rate VAT, the return on investment to society would be significant.

“We would also ask for consideration to be given as to whether this is an opportunity to further remove red tape and reduce ambiguity by allowing eligible bodies to claim zero rate VAT on all equipment used in research, treatment or training. Given the return on investment to society and the reduction in administration burden for suppliers and HMRC the benefits would outweigh the costs. HMRC would in turn only need to inspect the documents for the purchaser to ascertain adherence to the rules,” he says.

A version of this chart with working links can be downloaded from the GAMBICA website at www.gambica.org.uk

If you would like to support or be part of the campaign for all equipment used in research, treatment or training to be eligible for zero rate VAT, please contact me at [email protected]

Please note GAMBICA are not Tax advisors and accept no liability for the information provided. Each supplier should seek guidance from competent professional advisors regarding VAT tax and law and Suppliers need to come to their own conclusions as to the eligibility of an item for zero rate VAT. Please refer to guidance 701/6 and 701/1 for further advice.

Lab Asia 33.4 - August 2026

-(1).jpg)

.jpg)

.jpg)